Reserves

Not Federal and has no Reserves.

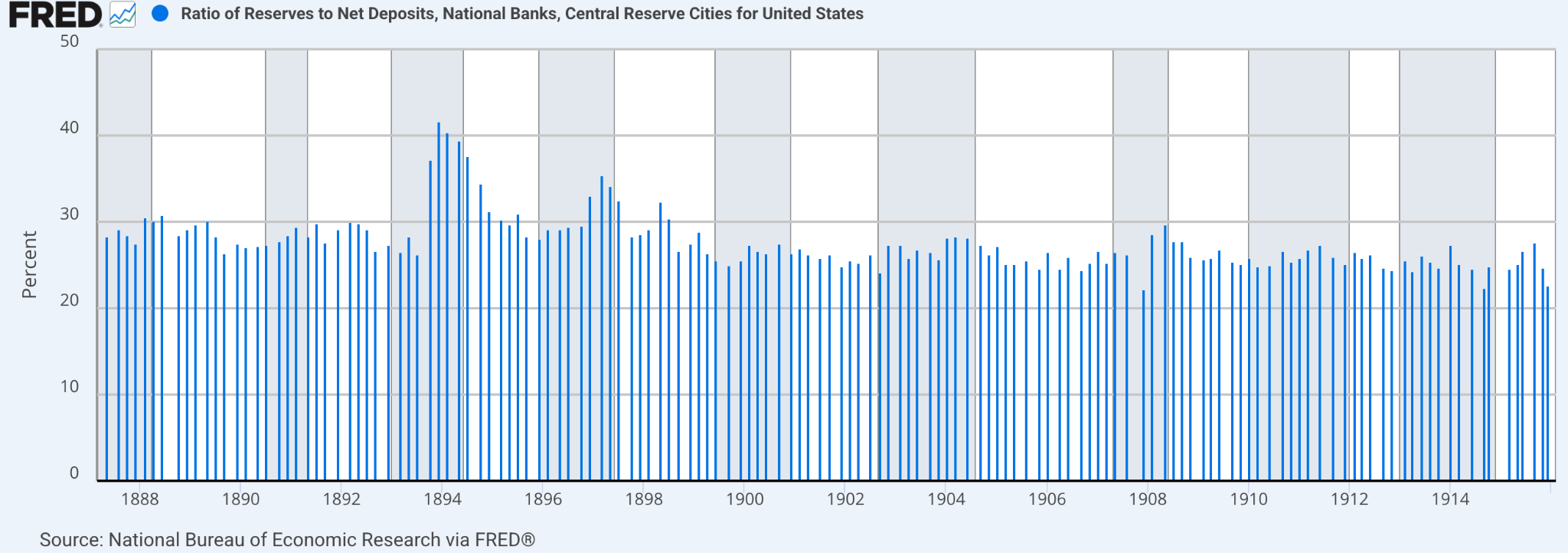

When we deposit money at the bank, the bank marks that deposit as a liability. To supplement this new liability, the bank loans out the money, creating an asset which balances out the deposit. Historically, as the bank loans out money, a reserve is kept in case the depositor needs their money back. This is a reserve ratio. The chart below shows the historic ratio from 1885 to 1915.

Before this time period, reserves were consistent around 30%, meaning that for every $100 you deposit, someone is currently utilizing $70 of your dollars while the bank holds $30.

After the Great Depression and creation of the Federal Deposit Insurance Corporation (FDIC), reserves ratios decreased through the 20th and early 21st century, down to 10%. In 2020, with the onset of Covid, the Federal Reserve reduced the reserve ratio requirements to 0%, allowing banks to loan out deposits an infinite amount of times.

As banks have more capacity to loan, they require more deals and in an ever more competitive state. The competition pushes yields down, forcing risk profiles to increase to achieve the same metrics as the year prior. Risk continues growing until investments inevitably bust, news of which leading to depositors demanding their cash back immediately.

In 2023, Silicon Valley and First Republic Banks both went under. They had heavily invested in US Treasuries at near 0% rates (true financial acumen). As yields increased and values dropped, depositors began demanding their money. The bank held the assets on their balance sheet at the face value of the bond instead of the market value, making it seem higher. It was when they needed liquidity to pay the depositors that they were forced to sell their underwater bonds for well below face value.

To quell the panic, because every bank in the Country had and still has these bonds and other loans held at face value instead of their pennies on the dollar market value, the FDIC stepped in and stated they would insure all deposits above the traditional $250,000 cap.

The FDIC came out and stated we will insure banks to the maximum extent to prevent any panic. The FDIC only has about $15B in cash, the other $115B being invested in the same securities as the banks, which are underwater on a market value. The cherry on top is that the FDIC’s total $130B is only enough to cover 1.4% of deposits…

This equivalent unrealized loss is currently happening at the Federal Reserve, where their market value is ~$1.1T in the hole. Fortunately for them, instead of needing to sell below face value, they can print infinite federal reserve notes when needed. We trade our finite time for something that is infinite; it doesn’t seem like a good deal to me.